Important Disclaimers

This article is for educational and informational purposes only and does not constitute legal, financial, or medical advice. Medicare rules, premiums, deductibles, and plan availability change annually. All figures cited below are based on 2025 official CMS data unless specifically labeled as “projected for 2026.” You should verify all information with 1-800-MEDICARE, your State Health Insurance Assistance Program (SHIP) , or a licensed Medicare broker before making any enrollment decision.

This content is not affiliated with or endorsed by the Centers for Medicare & Medicaid Services (CMS) or any government agency.

If you are approaching age 65 or retiring after 2025, you will face one of the most consequential financial decisions of your retirement: choosing between Medicare Advantage (Part C) and Original Medicare with a Medigap supplement.

The wrong choice can cost you thousands of dollars per year—and worse, it can lock you out of better plans if your health declines.

In 2025, the two most popular options are Medicare Advantage (private insurance replacing Original Medicare) and Original Medicare plus a Medigap Plan G (supplemental insurance covering most out-of-pocket costs). Both have legitimate use cases. But they operate on completely different financial models.

This guide compares them using official 2025 CMS data, explains what is projected to change in 2026, and gives you a decision framework based on your health, travel habits, and savings.

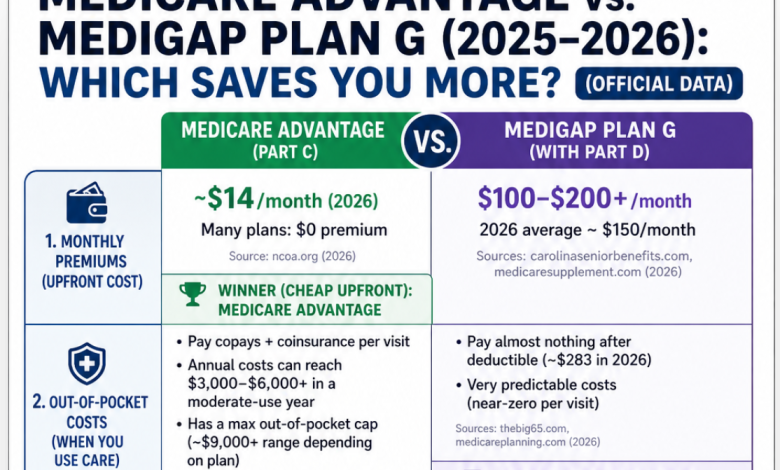

Summary Table (2025 Official Data)

| Feature | Medicare Advantage (2025) | Medigap Plan G (2025) |

|---|---|---|

| Monthly premium (national avg) | 19–55 (some $0-premium plans exist) | 140–190 (age 65, non-smoker) |

| Part A deductible ($1,676 per benefit period in 2025) | Varies; many plans waive it or charge 0–395/day copay | Plan G pays 100% after you meet Part B deductible |

| Part B deductible ($257 in 2025) | Varies; some plans waive it, most require 0–150 | You pay the first $257/year; Plan G pays 100% after that |

| Out-of-pocket maximum (in-network) | Varies; legal maximum is $8,850 in 2025 | No out-of-pocket maximum (plan covers 100% after deductibles) |

| Referral needed for specialist? | HMO: almost always yes; PPO: no | Never |

| Foreign travel emergency | Rarely covered (limited to urgent/emergency only) | Yes: 80% after 250deductible,50,000 lifetime limit |

| Best for… | Healthy individuals, low savings, urban HMO availability | Anyone with chronic conditions, travelers, those wanting predictable costs |

Key takeaway: Medicare Advantage saves you money in years you stay healthy. Medigap Plan G saves you money in any year you have a major hospitalization or chronic illness. Because 62% of 65-year-olds will have at least one hospitalization before age 75 (source: Kaiser Family Foundation, 2024 analysis), Plan G is actuarially safer for most retirees who can afford the premium.

What Changed in 2025? (Official Data)

Before comparing costs, you need the actual 2025 numbers. These are published by CMS and effective January 1, 2025.

2025 Medicare Deductibles and Premiums (Official)

| Item | 2025 Amount |

|---|---|

| Part B monthly premium (standard) | $185.00 |

| Part B annual deductible | $257.00 |

| Part A deductible (per benefit period) | $1,676.00 |

| Part A coinsurance (days 61–90) | $419.00 per day |

| Part A coinsurance (days 91–150 lifetime reserve) | $838.00 per day |

| Skilled nursing facility coinsurance (days 21–100) | $209.50 per day |

Source: CMS.gov, “2025 Medicare Parts A & B Premiums and Deductibles,” released October 2024.

Medicare Advantage 2025 Legal Limits

-

Maximum out-of-pocket (in-network): $8,850

-

Maximum out-of-pocket (in + out of network combined): $13,300

-

Average Medicare Advantage premium (all plans): $19.52/month

-

Zero-premium plans available in: 71% of U.S. counties

Source: CMS 2025 Medicare Advantage Landscape Analysis.

New for 2025–2026: Prior Authorization Rule

Effective January 1, 2025, the CMS Interoperability and Prior Authorization Final Rule requires Medicare Advantage plans to:

-

Provide prior authorization decisions within 72 hours for urgent requests

-

Provide decisions within 7 calendar days for standard requests

-

Publicly report denial rates

This does not eliminate denials—it only speeds up the process and adds transparency.

#1: Medicare Advantage (2025 Official)

How It Works

You enroll in Part A and Part B, then choose a private insurance company (UnitedHealthcare, Humana, Aetna, BCBS, etc.) to administer your benefits. The government pays that insurer a fixed monthly amount (approximately 1,100–1,300 in 2025) to manage your care.

Most Medicare Advantage plans are:

-

HMO (Health Maintenance Organization): Requires in-network providers and referrals for specialists

-

PPO (Preferred Provider Organization): Allows out-of-network care at higher cost, no referrals needed

Real 2025 Example (Harris County, Texas)

Plan: Aetna Medicare Explorer Premier (HMO-POS)

-

Monthly premium: $0

-

Annual drug deductible: $0 (Tiers 1–2)

-

Primary care visit: $0 copay

-

Specialist visit: $45 copay

-

Inpatient hospital stay (days 1–7): $395 per day

-

Inpatient hospital stay (days 8+): $0

-

Out-of-pocket maximum (in-network): $5,900

-

Maximum out-of-pocket (in + out of network): $9,800

Hidden cost reminder: Under an HMO plan, if you see an out-of-network specialist without a referral, you pay 100% of the bill.

Who Saves Money with Medicare Advantage?

Scenario A: Healthy retiree, no hospitalizations

Betty, age 67, takes one generic blood pressure medication (lisinopril). She sees her primary care doctor twice per year and a dermatologist once per year.

| Cost Item | Medicare Advantage | Plan G (for comparison) |

|---|---|---|

| Monthly premium (12 months) | $0 | 165×12=1,980 |

| Part B deductible | $0 (waived by plan) | $257 |

| Primary care (2 visits) | $0 | $0 after deductible |

| Specialist (1 visit) | $45 | $0 after deductible |

| Generic drugs (12 months) | 0–100 | Separate Part D plan (~$300/year) |

| Total annual cost | 45–145 | $2,537 |

Verdict: Betty saves approximately $2,400 per year on Medicare Advantage.

Who Loses Money with Medicare Advantage?

Scenario B: Chronic illness (colorectal cancer diagnosis)

Robert, age 72, enrolls in the same $0-premium Medicare Advantage HMO. In March 2025, he is diagnosed with colorectal cancer requiring surgery, chemotherapy, and skilled nursing facility rehab.

| Cost Item | Medicare Advantage | Plan G |

|---|---|---|

| Monthly premium (12 months) | $0 | 165×12=1,980 |

| Part B deductible | $0 | $257 |

| Hospitalization (5 days inpatient) | 395×5=1,975 | $0 |

| Oncologist visits (12 visits × $45) | $540 | $0 |

| Chemotherapy (Part B drug) | 0 after hitting 5,900 OOP max | $0 |

| Skilled nursing (days 21–30, 10 days × $209.50) | $2,095 | $0 |

| Total out-of-pocket | $5,900 (hits OOP max in June) | $2,237 |

Verdict: Robert pays 3,663 more on Medicare Advantage despite having a 0 premium.

#2: Medigap Plan G (2025 Official)

How It Works

You keep Original Medicare (Part A and Part B). The government pays 80% of approved amounts after deductibles. You then buy a Medigap Plan G policy from a private insurer that pays the remaining 20%, plus:

-

Your Part A deductible ($1,676 per benefit period)

-

Your Part A coinsurance (days 61–90 and lifetime reserve days)

-

Your skilled nursing facility coinsurance (days 21–100 at $209.50/day in 2025)

-

The first 3 pints of blood per year

What Plan G does NOT cover:

-

The Part B deductible ($257 in 2025)

-

Part B excess charges (only Plan G does NOT cover excess charges; Plan F does, but Plan F is unavailable to new enrollees after 2020)

-

Dental, vision, hearing, or prescription drugs

Real 2025 Costs (Standard Plan G)

Based on 2025 rate filings for a 65-year-old non-smoking male:

| Insurer | Monthly Premium (2025) | Annual Increase Cap |

|---|---|---|

| AARP/UnitedHealthcare (community-rated) | 149–169 | None (varies by state) |

| Mutual of Omaha (attained-age rated) | 142–158 | 3–6% per year |

| State Farm (issue-age rated) | 175–195 | Lower annual increases |

| Humana (attained-age rated) | 155–175 | 3–7% per year |

High-Deductible Plan G (2025):

-

Monthly premium: 55–85

-

Annual deductible (before Plan G pays anything): $2,800 (2025 figure)

-

After you pay 2,800out−of−pocket(includingthe257 Part B deductible), Plan G covers 100% of remaining Medicare-approved costs.

Who Saves Money with Plan G?

Scenario C: Major illness (stroke or heart attack)

Robert from the previous example chooses Plan G instead of Medicare Advantage.

| Cost Item | Plan G (Standard) |

|---|---|

| Monthly premium (12 months) | 165×12=1,980 |

| Part B deductible | $257 |

| Hospitalization (surgery) | $0 (Plan G covers Part A deductible) |

| Specialist visits (12×) | $0 |

| Chemotherapy | $0 |

| Skilled nursing (days 21–30) | $0 |

| Total out-of-pocket | $2,237 |

Verdict: Compared to Medicare Advantage (5,900),Robert∗∗saves3,663** with Plan G.

Scenario D: Three hospitalizations in one year

Mary, age 70, has congestive heart failure and is hospitalized three separate times in 2025. Under Original Medicare alone, she would pay three Part A deductibles (1,676×3=5,028). Under Plan G, she pays $0 for all Part A deductibles.

| Item | Plan G (Standard) |

|---|---|

| Monthly premium | 165×12=1,980 |

| Part B deductible | $257 |

| Part A deductibles (3× $1,676) | $0 (Plan G covers) |

| Total | $2,237 |

Under Medicare Advantage (with a 5,900OOPmax), Mary would pay 5,900

Verdict: Plan G saves Mary $3,663.

Side-by-Side Cost Comparison (2025 Official Dollars)

| Expense | Medicare Advantage (HMO example) | Medigap Plan G (Standard) | High-Deductible Plan G |

|---|---|---|---|

| Monthly premium (12 months) | 0–600 | 1,704–2,280 | 660–1,020 |

| Part A deductible ($1,676 per 60 days) | Hospital copay model (0–395/day) | $0 | 0after2,800 deductible |

| Part B deductible ($257/year) | Often $0 | $257 | Included in $2,800 |

| Skilled nursing (days 21–100 at $209.50/day) | 0–209.50/day | $0 | $0 after deductible |

| Foreign travel emergency | Rarely covered | 80% after 250deductible,50k lifetime | Same |

| Worst-case annual cost (major illness) | 5,900–8,850 | 1,961+257 = $2,218 | (85×12)+2,800 = $3,820 |

| Best-case annual cost (healthy) | 0–500 | $2,218 | (55×12)+257 = $917 |

The Doctor Network Problem

Medicare Advantage (2025 Data)

-

HMO plans: You are restricted to in-network providers. Out-of-network non-emergency care is not covered.

-

PPO plans: Out-of-network care is allowed but at higher cost (typically 30–50% coinsurance vs. 0–20% in-network).

-

Finding a cancer center: A 2024 Kaiser Family Foundation analysis found that 38% of Medicare Advantage HMO plans exclude at least one NCI-designated cancer center within 50 miles of a major metropolitan area.

Medigap Plan G

-

You can see any doctor or hospital in the U.S. that accepts Medicare (over 93% of providers).

-

No referrals required for specialists.

-

No prior authorization for most services (except for a small number of procedures requiring prior authorization under Original Medicare itself).

Who cares most about networks?

-

Retirees who split time between two states (snowbirds)

-

People with rare diseases needing specialized centers (MD Anderson, Sloan Kettering, Mayo Clinic)

-

Anyone who values direct access to specialists without waiting for a referral

Which One Actually Saves You More Money?

You save more with Medicare Advantage IF:

-

You are healthy with no expected hospitalizations in the next 3–5 years.

-

You have less than **10,000inliquidsavings∗∗(youcannotcomfortablyafforda150–$200/month premium).

-

You live in a dense urban area with multiple large HMO networks (e.g., Los Angeles, Chicago, Houston, Miami).

-

You do not travel out of state for extended periods (more than 2 months per year).

-

You are okay with prior authorization requests for expensive procedures and specialists.

Expected annual savings over Plan G (healthy years): 1,500–2,500

You save more with Medigap Plan G IF:

-

You have any chronic condition (diabetes, heart disease, COPD, rheumatoid arthritis, kidney disease, cancer history).

-

You want predictable, fixed costs with no surprise bills.

-

You travel or spend winters in another state.

-

You have at least $3,000 in annual budget flexibility for a higher premium.

-

You want to see specialists without referrals or prior authorization.

Expected annual savings over Medicare Advantage (sick year): 3,000–6,000

The Actuarial Reality

According to the Society of Actuaries (2023 study) :

-

A 65-year-old male has a 58% probability of entering a nursing home or having a major hospitalization before age 80.

-

A 65-year-old female has a 67% probability over the same period.

If you are in the majority who will have at least one major health event, Plan G is actuarially cheaper despite its higher premium.

The Medigap Enrollment Window

Your Medigap Open Enrollment Period is a one-time, six-month window that begins on the first day of the month you turn 65 AND are enrolled in Medicare Part B.

Important nuances:

-

If you delay Part B because you have employer coverage, your Medigap enrollment window does NOT start until you actually enroll in Part B.

-

During this window, insurance companies cannot deny you coverage or charge you higher premiums based on pre-existing conditions.

-

Outside this window: In most states, you must pass medical underwriting (health questions). If you have a pre-existing condition, you can be denied or charged substantially higher premiums.

Exception states (have annual or continuous open enrollment for Medigap regardless of health):

-

Connecticut

-

Maine

-

Massachusetts

-

New York

-

Vermont

-

Washington (some restrictions apply)

Action step: If you want Plan G, enroll during your initial six-month window. Waiting until after a health crisis may lock you out permanently.

Projected Changes for 2026

The following are estimates based on historical trends and CMS advance notices. These are not final.

| Item | 2025 Actual | 2026 Projected (as of May 2025) |

|---|---|---|

| Part B monthly premium | $185.00 | 190–200 |

| Part B deductible | $257 | 260–275 |

| Part A deductible | $1,676 | 1,700–1,740 |

| Skilled nursing daily coinsurance (days 21–100) | $209.50 | 215–225 |

| Medicare Advantage maximum OOP (in-network) | $8,850 | 9,000–9,200 |

| High-deductible Plan G annual deductible | $2,800 | 2,900–3,000 |

Sources: CMS Advance Notice for 2026 (released February 2025), Medicare Trustees Report 2025.

Our recommendation: Use 2025 numbers for decision-making today. Re-evaluate during the Annual Enrollment Period (October 15 – December 7, 2025) when 2026 official numbers are published.

Frequently Asked Questions

Q: Can I switch from Medicare Advantage to Medigap without medical underwriting?

A: Generally, no. In most states, after your first 12 months in Medicare Advantage, you must pass health questions to buy a Medigap policy. Exceptions: you move out of your plan’s service area, your plan leaves the market, or you live in one of the six exception states listed above.

Q: Does Plan G cover dental, vision, or hearing?

A: No. You need separate dental/vision policies or a standalone Part D plan for prescriptions. Medicare Advantage plans often include limited dental (up to 1,500/year),vision(200 for glasses), and hearing aids (500–1,000 per ear).

Q: What is the “Part B Giveback” benefit?

A: Some Medicare Advantage plans (called “MSA plans” or certain HMOs) reduce your Part B premium by up to 150/month.Forexample,ifyourPartBpremiumis185, a 100givebackmeansyoupayonly85. This does not change network restrictions or out-of-pocket maximums.

Q: Is Plan G better than Plan N?

A: Plan N has lower premiums (typically 20–40 less per month) but requires you to pay:

-

Up to $20 per doctor visit

-

Up to $50 per emergency room visit (waived if admitted)

-

Part B excess charges (if a doctor does not accept Medicare assignment)

Plan G has higher premiums but no copays for visits. For frequent doctor users, Plan G is cheaper.

Action Steps for 2025–2026 Enrollment

-

Confirm your Part B effective date by logging into your SSA.gov account or calling 1-800-772-1213.

-

Use the official Medicare Plan Finder at Medicare.gov/plan-compare. Enter your specific drugs and doctors. Do not rely on general guides.

-

Call your State Health Insurance Assistance Program (SHIP) for free, unbiased counseling. Find yours at shiphelp.org.

-

If you choose Medigap Plan G, enroll during your initial six-month window. Mark your calendar. Missing this window can cost you thousands or lock you out entirely.

-

If you choose Medicare Advantage, verify that your preferred hospital and cancer center are in-network. Call the plan directly and ask for a written directory.

Final Verdict

| Your profile | Best plan | Estimated 2025 total (healthy year) | Estimated 2025 total (sick year) |

|---|---|---|---|

| Healthy, low income (<$30k/year), urban | Medicare Advantage ($0 premium HMO) | 0–500 | 5,900–8,850 |

| Healthy, $50k+ savings, travels frequently | Plan G (standard) or High-Deductible G | $2,218 | $2,218 |

| Moderate health, wants flexibility | Plan G (High-Deductible) | $917 | $3,820 |

| Any chronic condition | Plan G (standard) | $2,218 | $2,218 |

| Turning 65 with pre-existing condition (diabetes, heart disease, cancer survivor) | Plan G (standard) | $2,218 | $2,218 |

If you can afford the monthly premium of Plan G, buy it. The peace of mind and protection against catastrophic out-of-pocket costs are worth the extra 1,500–2,000 per year for the majority of retirees who will eventually need significant medical care.

Sources

-

Centers for Medicare & Medicaid Services. (2024). 2025 Medicare Parts A & B Premiums and Deductibles. CMS.gov.

-

Centers for Medicare & Medicaid Services. (2024). 2025 Medicare Advantage and Part D Landscape Analysis. CMS.gov.

-

Kaiser Family Foundation. (2024). Medicare Advantage Network Adequacy: Access to Cancer Centers. KFF.org.

-

Society of Actuaries. (2023). Long-Term Care and Hospitalization Probability Tables. SOA.org.

-

Medicare Payment Advisory Commission (MedPAC). (2025). Report to Congress: Medicare Advantage Payment Policy.